Unrelated Business Income Tax (UBI) Criteria

Directive Statement

If the University of Florida carries on a trade or business that is not substantially related to its exempt purpose, the University is subject to tax on its income from the unrelated trade or business; hence, unrelated business income (commonly referred to as UBI).

Remember – the IRS is concerned with how the funds are generated, instead of how the funds are used!

Reason for Directive

To ensure University of Florida compliance with all applicable IRS requirements.

Who must comply?

All UF departments.

Criteria

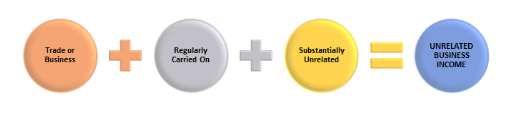

For income to be unrelated business income and taxable, the activity generating the income must meet all 3 criteria:

Be conducted as a trade or business

Activities cannot be considered taxable unless they are deemed to be a “trade or business” as defined in IRC Section 162. Among other things, a trade or business must exhibit intent to profit from the activity (real economic profit).

If the intent is to merely recover costs and indeed no realized profit exists, the activity lacks a profit motive and is not subject to taxation.

In addition, there must be a regularity of activities and income production that would be different than the level of activity found in a hobby-like activity. (IRS Treasury Regulation 1.513-1(b)).

Be regularly carried on

The IRS Treasury Regulations consider the frequency and continuity of the activity and the manner in which it is pursued to determine if the activity is regularly carried on. Thus, the unrelated business income tax (UBIT) applies only to a business activity which is regularly carried on as distinguished from commercial transactions which are sporadic or infrequent. (IRS Treasury Regulation 1.513-1(c)(1)).

An activity should not be considered as regularly carried on if it is:

- on a very infrequent basis;

- for a short period of time during the year; or

- without competitive and promotional efforts

Activities over a period of only a few weeks are not “regular” for an exempt organization if the activities are of a kind normally conducted by a nonexempt business on a year-round basis. Intermittent, casual, or sporadic activities are generally not regular.

However, year-round activities are regular even if they are conducted only one day a week. Further, seasonal activities may be regularly carried on even though they are conducted only for a short period each year. (IRS Treasury Regulation 1.513-1(c)(2)).

The IRS expanded its definition of time-period with the court case National Collegiate Athletic Association vs. Commissioner in July 1991 which looked at the duration of the event itself and not the preparation time involved.

Substantially unrelated to the tax-exempt mission of the University

To be a related activity, the conduct of the activity must contribute importantly to achieving a tax-exempt purpose. (IRS Treasury Regulation 1.513-1(d)(2)). How the funds are used is not a factor. The mere fact that an activity generates a source of funds that are then used to carry out a mission-related activity does not mean that the activity is related to the mission.

The University’s tax-exempt purposes include education, research, lessening the burdens of government, and others. Characterizing a business activity as a related business requires an analysis that shows how conducting the activity — i.e., how selling the goods or performing the services – contributes importantly to accomplishing the University’s exempt purposes.

Conducting an activity on a larger scale than is necessary to achieve a tax-exempt purpose could also result in UBI, as could charging fees to the general public equivalent to what a commercial business would charge.

Particular emphasis is placed on the size and extent of the activity. If an activity is conducted on a scale larger than reasonably necessary to carry out the exempt purpose, it is more likely to be treated as unrelated. (IRS Treasury Regulation 1.513-1(d)(3)). Use for both exempt and commercial purposes will not necessarily exempt the income derived from commercial use unless the business activity “contributes importantly” to the accomplishment of exempt purposes. (IRS Treasury Regulation 1.513-1(d)(4)(iii)).

Exclusions

There are possible exclusions, exceptions and modifications for each of these criteria depending on the activity in question. Activities that are determined to produce unrelated business income/loss (UBI) will be included in the University’s Exempt Organization Business Income Tax Return (Form 990-T), to be prepared each year for submission to the Internal Revenue Service.

UBI Definitions

The UBI Definitions page provides definitions of terms used in determining UBI.

Last Reviewed

Last reviewed on 06/28/2024

Resources

IRS Publication 598, Tax or Unrelated Business Income of Exempt Organizations

Contacts

Auxiliary Accounting: (352) 294-7236

Tax Services: (352) 294-7266